In a context of tight budget constraints and the pursuit of sustainable savings, the French government is considering adopting new budget management methods starting in 2026. Among them, Zero – Based Budgeting (ZBB) — a practice already well-established in large American corporations — is gaining attention for its rigor: every expense must be justified, with no automatic renewals. This logic offers inspiration for CIOs, who also face the need to rethink how they allocate resources.

Traditional budgeting methods, theorized as early as the 1920s by McKinsey, relied on a historical logic of expense lines, adjusted marginally year after year.

This model was challenged in the 1970s with the rise of cost-cutting strategies, a period during which companies began focusing more on budget optimization. It was in this context that Zero-Based Budgeting (ZBB) emerged as a more radical alternative, encouraging a complete re-evaluation of each budget line from scratch. Jimmy Carter even advocated for it: “If I am elected president, I will implement ZBB, which evaluates every program each year and eliminates those that are obsolete.”

Since 2010, this approach has evolved to incorporate a value-oriented dimension, and according to an Accenture study (2019), 90% of large companies now use it to optimize costs.

But is ZBB really the only effective method? What other budgeting approaches are CIOs adopting to combine financial discipline with value creation?

In this article, we will detail and compare the various methodologies that a CIO office can adopt to manage and optimize its budget. Specifically, we will discuss the traditional budgeting approach, the Zero – Based budgeting method and its agile alternative Agile Zero – Based Budgeting, the Activity – Based Costing method, and the IT Fitness methodology developed by Wavestone.

Does the traditional budget optimization method still meet CIO challenges?

The traditional method — based on adjusting the previous year’s budget by a fixed percentage — is easy to implement and predictable for planning. However, it quickly shows its limits in today’s fast-changing IT environments. It lacks flexibility, fails to challenge existing expenses, and is not responsive enough to support strategic business shifts. Yet, CIOs today must:

- Align with the company’s business strategy to ensure that adopted technologies support business goals coherently

- Ensure reliable budget management through value-based decision-making

- Improve financial forecasting models to support strategic IT decisions

- Reduce and optimize the IT costs by rationalization of providers, applications, IT assets (servers, workstations, mobiles, …) and usage of new technologies (RPA, IA, Cloud, etc.)

These imperatives require dynamic, agile, and data-driven budget management, something the traditional method cannot fully provide. It is therefore crucial to adopt more modern budgeting approaches that integrate a strategic and collaborative vision of IT management.

What methodological alternatives address today’s CIO challenges?

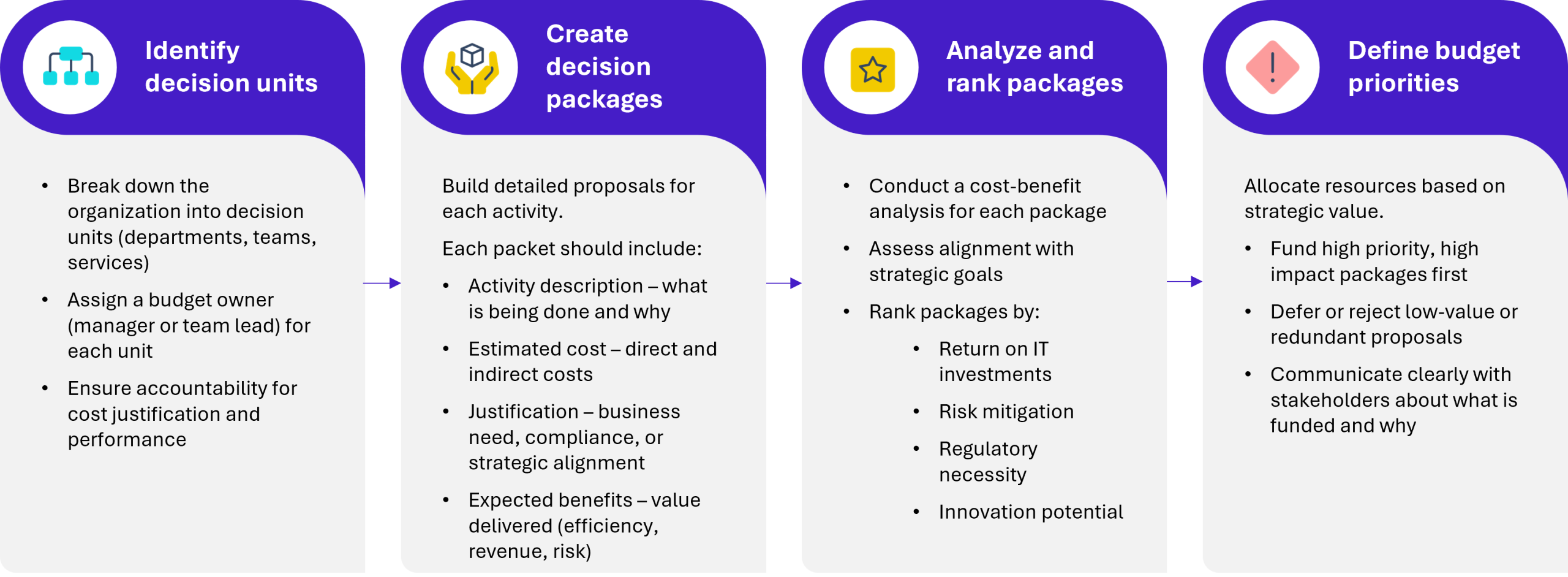

Zero-Based Budgeting (ZBB) stands out as a rigorous alternative to the traditional method. Unlike the latter, which relies on historical data, ZBB requires full justification of each expense item from scratch every year. This method promotes greater cost transparency, reduces unnecessary spending, and ensures optimal resource allocation. It follows several key steps, illustrated in the diagram below:

Figure showing the different steps of the ZBB methodology

However, ZBB can be burdensome to implement, requiring time, appropriate tools, and strong team involvement.

To meet the agility demands placed on CIOs, an evolved version, Agile Zero-Based Budgeting (AZBB), combines ZBB’s rigor with decision-making flexibility. This method allows for rapid budget adjustments based on shifting priorities, while involving managers more in budget trade-offs, enhancing responsiveness and strategic alignment. It typically relies on short cycles (quarterly or monthly), fostering an iterative and collaborative approach. In practice, AZBB is particularly suited to dynamic or multi-project environments where resources must be quickly reallocated based on added value.

Other approaches, such as Activity-Based Costing (ABC), offer a detailed cost analysis based on value-generating activities. It helps to better understand IT service profitability but requires fine mapping and regular process updates. ABC identifies low-value activities, often invisible in traditional accounting, and helps rationalize efforts accordingly. It is effective in contexts with high or complex indirect costs (especially in large multi-service IT departments).

Finally, the IT Fitness method, developed by Wavestone, is a structured approach aimed at enhancing the economic performance of IT departments. It does so by identifying, prioritizing, and activating high-impact optimization levers, while ensuring rigorous governance of cost-saving initiatives.

Far beyond a simple cost-cutting exercise, IT Fitness provides a comprehensive and structured view of IT spending, enabling organizations to rapidly identify areas with high savings potential. It is adaptable to all levels of IT maturity and integrates benchmarks and real-world experience to guide decision-making.

For several of our clients, we’ve integrated a FinOps approach as a concrete lever for IT Fitness —optimizing cloud consumption and controlling costs. But IT Fitness goes further by addressing the “people” and “process” dimensions by:

- Engaging IT teams around a culture of performance and accountability

- Structuring processes to better align IT with business priorities.

- Fostering collaboration between IT, procurement and finance

Moreover, the methodology’s key optimization levers include:

- Rationalizing architecture

- Optimizing actual infrastructure usage:

- Resizing: recalibrating infrastructure to match real usage and reduce overcapacity

- Shutting down unused machines at night or during off-peak hours

- Instance reservations: pre-purchasing cloud resources at discounted rates

- Cost allocation

- Raising team awareness of IT financial issues

However, this methodology can create internal tensions, as some recommendations involve significant cuts, including human resources.

Which method best meets today’s CIO challenges?

Given the detailed descriptions of these methodologies, it is necessary to place them in a broader comparative framework to assess their relevance considering growing demands for agility, value-driven management, and resource optimization within IT departments.

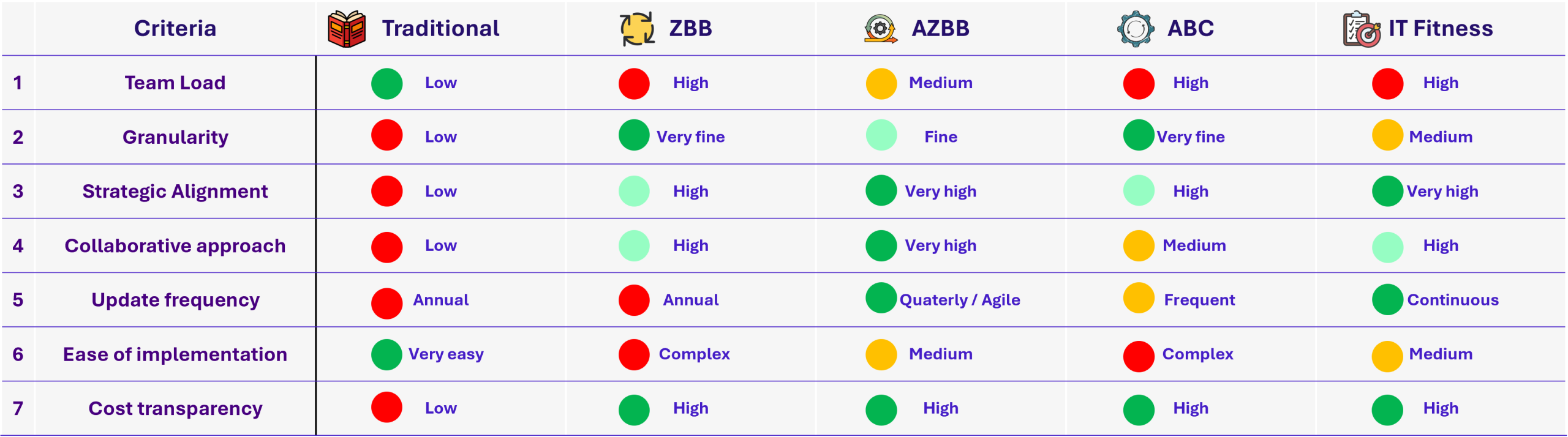

The table below offers a multi-criteria comparison of the main budgeting methodologies across key dimensions such as team workload, granularity, strategic alignment, update frequency, and cost transparency. These criteria are not random, they reflect modern organizations’ expectations for responsiveness, efficiency, shared governance, and financial control:

- Team load: this criterion matters because it measures the effort required from teams to implement the methodology

- Granularity: it indicates the level of detail in cost analysis. The finer the granularity is, the better the precision is

- Strategic alignment: it shows how well the method supports business goals. It is crucial in determining long-term value

- Collaborative approach: it reflects how much the method involves cross-functional teams

- Update frequency: it reflects how often the budget or cost model can be revised

- Ease of implementation: it indicates how complex the method is to deploy

- Cost transparency: it measures how clearly costs are traced to activities or value

Table comparing the different methodologies based on several criteria

Considering these criteria, the traditional method shows serious limitations: it is not very collaborative, poorly aligned with strategy, and rigid in its updates — its only advantage being ease of implementation.

Conversely, AZBB and IT Fitness stand out for their strong strategic alignment, transparency, and enhanced collaboration.

ZBB, while strategic and detailed, suffers from its complexity. ABC is rich in data but remains burdensome to implement. Finally, IT Fitness appears to be the most balanced: sufficiently agile, collaborative, continuously updated, while maintaining good cost clarity. It thus effectively meets the demands of modern and agile management.

In conclusion, in increasingly complex and fast-moving technological environments, CIOs must adopt budgeting methods that are rigorous, agile, and value oriented. While AZBB and IT Fitness currently appear to be the most comprehensive approaches, no model is universal: the choice depends on the level of maturity, strategic objectives, and culture of each organization. In fact, AZBB and IT Fitness offer the best strategic alignment and collaboration, ideal for agile organizations. ZBB and ABC provide high granularity, but at the cost of team.

Now, the question remains open: how can these methodologies evolve to meet the future challenges of ever-changing technological environments?

Sources :